Interest rates are still low. As a result, we are increasingly asked if it makes more sense to invest extra cash rather than pay down debt. The same question comes up when we recommend using non-registered investments to pay down debt.

You might be thinking:

“If my mortgage rate is under 3%, wouldn’t I be better off investing extra cash and pocketing the difference?”

Maybe.

Let’s assume for the moment that leveraged investing is appropriate for you – because that’s what you would be doing. Further on, I’ll give you a checklist to determine if you really are a candidate for leveraged investing.

Let’s try an example

To start, let me challenge your assumption with a little math. We’ll assume you have $100,000 that you now want to invest, and you also have:

$220,000 mortgage or secured line of credit, with a 2.9 guaranteed interest rate

Investment return of 6% (not guaranteed) in a balanced portfolio; 2% interest, 2% dividends, 2% realized capital gains

$105,000 earned income in Ontario (marginal tax rate is therefore approx … 43%)

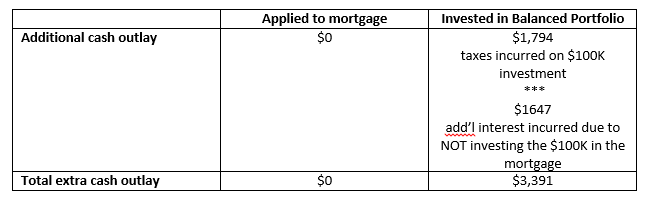

Difference in return: pay down mortgage debt or invest (own source)

Difference in cash flow: pay down mortgage debt or invest

The results

In this case, the choice of investing vs paying down the mortgage earns an extra 1.3% per year (4.2% – 2.9%). Note that if the portfolio return had a greater component of interest, taxes paid would be higher, decreasing the 1.3% advantage to investing that this case shows.

Of course, you could achieve a higher return on your investments, but you could also experience a lower, or negative return in the short term. In addition, you’ll want to pay the tax out of your bank account rather than withdrawing from your investment portfolio. Using your portfolio to pay taxes reduces the magical advantages of compound growth over time.

How do you stack the numbers in your favour?

Here are three ways to optimize your choices:

- Let the tax act help you. CRA lets you deduct your borrowing costs (interest charged) when you borrow to invest in an income generating investment. Note that the paper trail is important to qualify for the deduction. In our example, you would need to take the $100K cash and pay down your debt first, then borrow it back and invest in the portfolio. You must be able to prove that the borrowed funds were used to make the eligible investment.

- Invest tax-efficiently. The less taxable income the portfolio generates the better.

- Invest for growth. The higher return the better. Conservative fixed income won’t generate the returns you need to make this work, and is tax-inefficient to boot.

Checklist for leveraged investing

So, is this for you? Here’s the checklist I promised earlier, to decide whether you are a candidate for leveraged investing. See how many you say yes to!

- You are investing for the long term.

- You have a stable income and can afford to pay the annual loan interest and taxes on portfolio income from your cash flow rather than the portfolio.

- You will not have future borrowing needs. The leveraged strategy could impede your ability to borrow additional funds for other purposes.

- You have a high risk tolerance. This is necessary for two reasons:

A growth portfolio is necessary to generate the necessary return to compensate for the risk of the overall strategy.

Aborting the strategy during a bear market amplifies your losses. There is a loss on the investment as well as the outstanding debt that cannot be fully repaid when the strategy is unwound.

How did you do?

What can go wrong?

You’re a knowledgeable investor; before you make your choice, you want to review the downside as well. Here are the two eventualities most likely to derail a leveraged investing plan:

- Interest rates rise – rising loan interest rates and a stock market correction would be a bad combination. Historically, rising interest rates signal the end of an economic cycle, and precede a recessionary period, which is negative for the stock market.

- You need to liquidate the portfolio at an inopportune time. There are lots of reasons why you might need the cash. Job loss, supporting children or parents unexpectedly, and major house repairs are just some of the events that could force you to liquidate your investment at a time that undermines the leveraged strategy.

Is the risk worth it?

I always like to measure the long-term impact of investing versus debt repayment with a detailed financial planning exercise. You might be surprised to find out that paying down debt is the most effective, certain path towards your wealth-building goals.

But if you answered yes to all of the items in the checklist above, that risk of leveraged investing may be worth it for you. Talk to your advisor!

This information is of a general nature and should not be considered professional advice. Its accuracy or completeness is not guaranteed and Queensbury Strategies Inc. assumes no responsibility or liability.