“When I was born the doctor came out to the waiting room and said to my father “I’m very sorry. We did everything we could, but he pulled through.”

– Rodney Dangerfield

Poor Rodney. Never got any respect. Kind of like annuities.

There are a few reasons why annuities don’t get the attention they deserve. But first, a basic explanation of the product.

- An annuity is a contract that you make with an insurance company.

- You have savings.

- You give some of your savings to an insurance company in exchange for a guaranteed income for life. It’s kind of like a pension plan.

- You create your own “pension” by purchasing an annuity.

Most people love the idea of a guaranteed income for life. In fact, there are financial products that have been created to look like annuities, and these products became more popular than annuities themselves. Why is this?

They aren’t popular with advisors

- Annuities are sold, not bought – There aren’t investors lining up to buy annuities. It really takes an advisor who sees the benefit of an annuity for a client to strongly recommend that an annuity makes sense, at least in part, to fund retirement.

- It’s an insurance product – If your financial advisor isn’t licensed to sell insurance products, they may not bother to suggest annuities.

- Compensation conflict of interest – An annuity at the time of purchase will pay the salesperson about 1.5% commission at point of sale. It pays that commission only once. Whereas if that same amount of money was invested in a managed portfolio, where the advisor was charging 1% a year, the advisor would be receiving 1% a year, every year, for as long as that portfolio is being managed. That could be 10 years 20 years 30 years or longer. So you can see how much more lucrative it is to manage a portfolio at 1% a year than to recommend annuity that pays 1.5% just once.

They aren’t popular with investors

- Lack of liquidity – You can’t access to the capital used to buy the annuity. You do get the guaranteed income stream, but like a pension plan, if you needed an extra $10,000, for whatever, you can’t go the the insurance company and ask for an extra $10,000. That’s why, generally speaking, it’s not wise to invest every dollar you have in an annuity other sources, you will need to have a liquid pool of capital to draw from. the annuity strategy.

- Interest rates are too low – Most investors compare an annuity strategy with a guaranteed investment certificate strategy(GICs) because they are both guaranteed, hassle-free investments. Investors assume that if annuity rates are similar to GIC rates. The mistake that’s being made in that thinking is that the income stream that you receive from an annuity isn’t entirely based on interest rates. It also has to do with expectations about how long you will live. Your age matters. The income you get from an annuity is a combination of interest and return of your capital. So investors are often very surprised at how much cashflow they can get from an annuity as compared to a GIC.

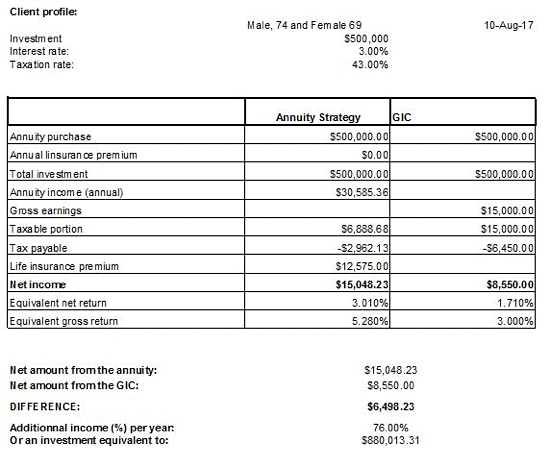

- Bad for beneficiaries – When you die, the income stops, and the capital is gone. So the idea that there would be nothing remaining of that original investment for your estate is extremely troubling for some people. You can mitigate that risk by through payment duration guarantees and/or through an insured annuity strategy.

Here is an example of how it works. (source: Hub Financial)

It’s hard to see why investors don’t at least consider this option as part of their retirement cash flow plan. Be fully informed. Ask your advisor to run some quotes for you.

This information is of a general nature and should not be considered professional advice. Its accuracy or completeness is not guaranteed and Queensbury Strategies Inc. assumes no responsibility or liability.