Following several years of above average equity market returns, it is time to take a step back and reset our expectations for returns over the next 5 to 10 years. This is because investor expectations for future returns are typically based on their recent experience. In behavioral finance terms, this is called the “recency effect”. This usually leads to two fateful investing mistakes – chasing returns, and ignoring your risk tolerance.

We can address behavioural finance in a future post. Today we will comment on why we expect returns over the next five years to be lower than the last five years, and it’s not why you might expect. It’s not because of the debt crisis in Greece. It’s not because of the rise of ISIS and the threat of increased geopolitical instability. It’s not because of any headline issue that you might read in the daily newspaper. It’s because……wait for it……security prices are fully valued and in the case of long term bonds, overvalued.

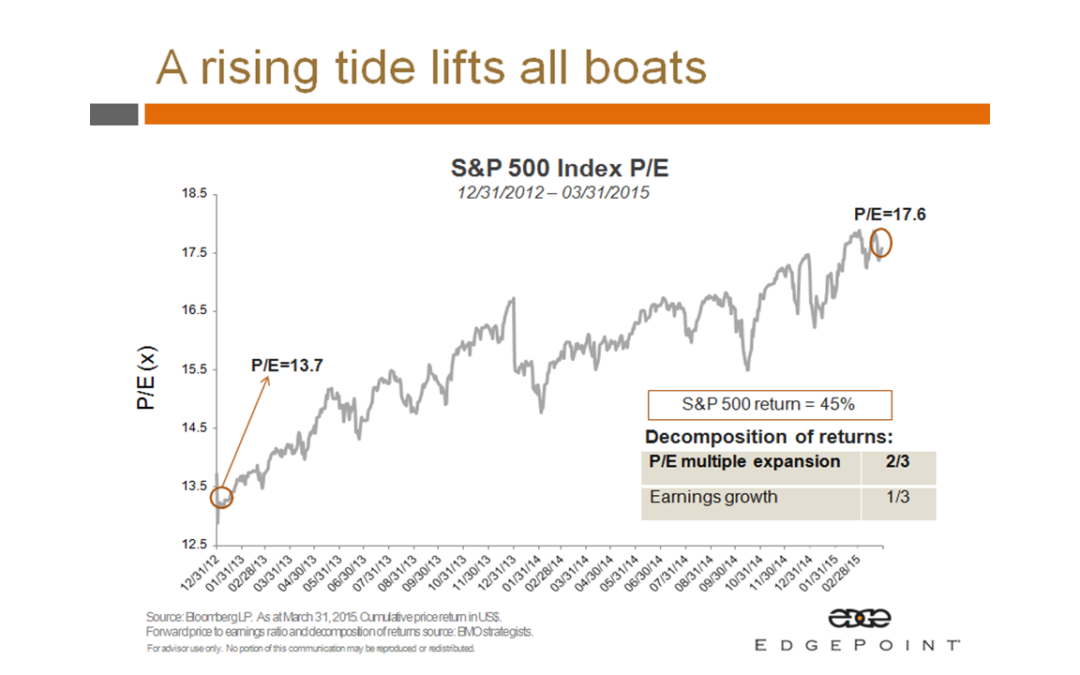

The pleasing returns that investors have enjoyed over the past five years (with a hiccup in 2011), was driven largely by something called “multiple expansion”. Multiple expansion occurs when investors value a company’s earnings more highly and will pay more for them. When investors become more attracted to something, like equity mutual funds for example, demand for the securities that those funds own grow, and the value of those holding increase even if the profits generated by those holdings don’t change. Nothing has really changed, but the investor has made money on the appreciation. As you can see from the chart below over the past two years, a full two thirds of the rise in the S&P 500 (US stock market) was due to multiple expansion and only one third was driven by earnings growth. This is not a bad thing. It simply reflects the fact that after the financial crisis of 2008/09, equity values were extremely undervalued.

So, where are we now? In our view global equity fund returns will moderate somewhat and become more closely tied to the rate of growth in company earnings. As you can see in the chart below, the S&P 500 is trading slightly above the average price/earnings multiple over the past 35 years.

That makes it more important than ever to have your equity allocation actively managed in professionally managed funds, where the portfolio managers can hand pick the best valued companies with the growth profile necessary to drive returns. Multiple expansion will likely not deliver, and in fact, may contract. As a result, index investing could be very disappointing over the next 5 – 10 years.

Also, we anticipate that after an extended period of declining interest rates in the bond market and therefore increasing bond prices, interest rates will likely stabilize and slowly rise, which would detract from bond performance.

Finally, volatility is sure to increase relative to the recent past. Equity market volatility over the last few years has been markedly lower than average, and that is probably a temporary aberration.

We liken the investment climate over the past 5 years to riding your bike downhill.

The wind is in your hair, and you feel like you will get to your destination in no time flat. “Wheeeeeeee!” But hills inevitably bottom out and turn uphill.

Riding uphill takes more effort, and is not nearly as enjoyable, but if the destination is worthwhile, retirement security for example, your focused effort will pay off.

At this time it is essential that you have a clear strategy for how both your overall financial planning and investment approach needs to respond the current environment. You need to decide now, what you will do when volatility returns and what adjustments you should make to either saving or spending patterns in the event that future returns are lower than the recent past.

This information is of a general nature and should not be considered professional advice. Its accuracy or completeness is not guaranteed and Queensbury Strategies Inc. assumes no responsibility or liability.