Lucky Americans – they pay much lower investment advisory fees than we do in Canada.

Or so many people think … but is it true?

With the new CRM2 legislation showing investors how much you pay for advice, it’s considerably easier to do a cross-border comparison. Let’s start with the two components of the fees you pay. And a heads-up – read this part twice! Most people don’t understand the two-component aspect of how financial advice is priced; you’ll be well ahead if you do.

Two components to fees

1. If you are working with a financial advisor, there are two components to the fees you pay, product and advisor:

- Product cost – the cost of the investments recommended by your advisor, e.g.

- Fund management portion of a mutual fund Management Expense Ratio (MER)

- MER of an ETF

- Trading costs

- MER of a pooled fund or segregated fund

2. Advisor cost – the cost of professional advice

- Service fee portion of a mutual fund MER

- Percentage charged by a fee-for-service financial advisor

- Flat fee or hourly fee charged by a fee-for-service financial advisor

Fee insights from a U.S. benchmarking study: the results may surprise you

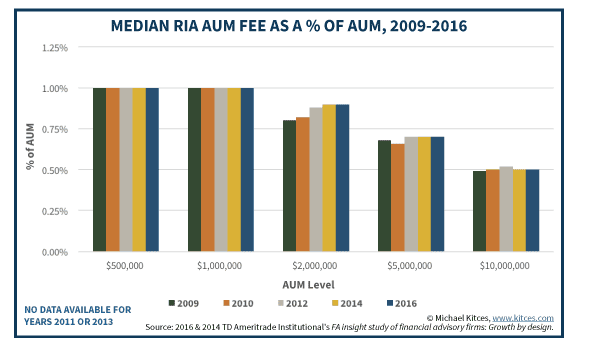

FA Insight recently released its 2016 financial advisor benchmarking study: Growth By Design. The latest information on fees might surprise you.

Since 2009 the median US advisory fee (not including product costs) on assets under management has hovered close to 1%. Fees drop to .70% at $5,000,000 and to .50% at $10,000,000 +.

But despite the fee pressure exerted by the robo-advisor trend, which took off in earnest in 2012, the 2014 edition of the FA Insight indicated that 70% of firms planned to keep their fees steady and 28% of firms planned to raise fees in the next two years. The data from 2016 confirmed the rise: 34% actually did raise fees.

So, do we pay more in Canada?

I believe that fees are somewhat higher here than in the US. This is based on both ongoing anecdotal evidence and data from the Globe and Mail Fee Tool (available to Globe Unlimited subscribers).

For example, I used the fee tool to find the average advisory fee being reported by Canadians with a portfolio between $500,000 and $1 million. 30% reported paying between 1.0 – 1.24% and 38% pay between 1.25% – 1.74%.

That is well above the 1% being charged in the US. Canadian investors are paying more relative to our US counterparts – it looks like the prevailing wisdom is correct!

The really big question – is it worth it?

It’s a matter of personal judgment as to whether you are receiving sufficient value for the fees you pay. However, at the very least, if you work with a financial advisor, you should know how their fees fit in the marketplace.

And even if the fees being charged by your advisor are competitive, you still need to evaluate whether you are getting value from the relationship.

The breadth and depth of service you receive depends on both the firm you deal with and the specific advisor. Some firm cultures encourage and reward holistic planning and advice; others pressure their advisors to focus on asset-gathering and reaching annual fee generation targets. What kind of firm do you think yours is?

Individual advisors differ as well. Some focus narrowly on investment management and advice. Others see their role more broadly, as financial planners, with a mandate that expands well beyond investment portfolio design and rebalancing.

In my mind? Premium pricing is appropriate only when you, the client, have access to advice that extends well beyond investment portfolio design.

This information is of a general nature and should not be considered professional advice. Its accuracy or completeness is not guaranteed and Queensbury Strategies Inc. assumes no responsibility or liability.